They keep arriving with open arms and leaving with your wallet. That’s not an accident. It’s a playbook.

You notice it only in retrospect, and with increasing frequency. A tool you’d started to take for granted, something you’d quietly woven into your process, turns out to have been in a probationary period all along. It seems the welcome invitation had an expiry date.

A pricing update arrives. The feature you’d come to depend on is still there, technically, but now it’s rationed, gated, or sitting behind a separate subscription tier you didn’t budget for. You’re not locked out. Just nudged, repeatedly, toward spending more.

This isn’t new behaviour in software. But with AI, the pace and the stakes have both increased. The costs of running large language models are genuinely high, the pressure to monetise is intense, and the credit-based pricing model has become the industry’s preferred tool for threading that needle. The result is a market in which “access” and “meaningful access” have quietly become two different things, and where freelancers and small teams are absorbing the friction that enterprise budgets simply write off.

We’ve been here before

To understand what’s happening with AI credits, it helps to watch the same company do it twice.

When Figma introduced Dev Mode at its 2023 Config event, it arrived as a free beta. The pitch was straightforward: a dedicated space for the designer-to-developer handoff, making it easier for engineers to inspect components, extract specifications, and follow along with what designers were building. Developers started using it. Workflows adapted around it. It became part of how cross-functional teams operated.

Then the beta ended. Dev Mode became a paid add-on, priced at $25 per seat per month on the Organisation plan and $35 on Enterprise. Simultaneously, Figma stripped back the previously free Inspect panel, the simpler tool that developers had been using for years, so that the more capable functionality now sat squarely behind the new paywall. It wasn’t that Dev Mode didn’t offer value; it was that the free alternative had been deliberately degraded, then removed, to make the paid version feel necessary.

The community backlash was significant. Forum threads ran to hundreds of replies. Comparisons to Adobe’s pricing practices, unflattering ones, circulated widely. Users noted the particular sting of a feature introduced for free, allowed to bed into professional workflows, and then monetised once dependency had formed. Some smaller agencies began weighing up alternatives like Penpot. Enterprise teams reported that the licensing costs for developer seats were, in some cases, doubling their annual Figma spend.

That was 2023. Fast forward to 2025, and Figma ran the same play again. This time with AI.

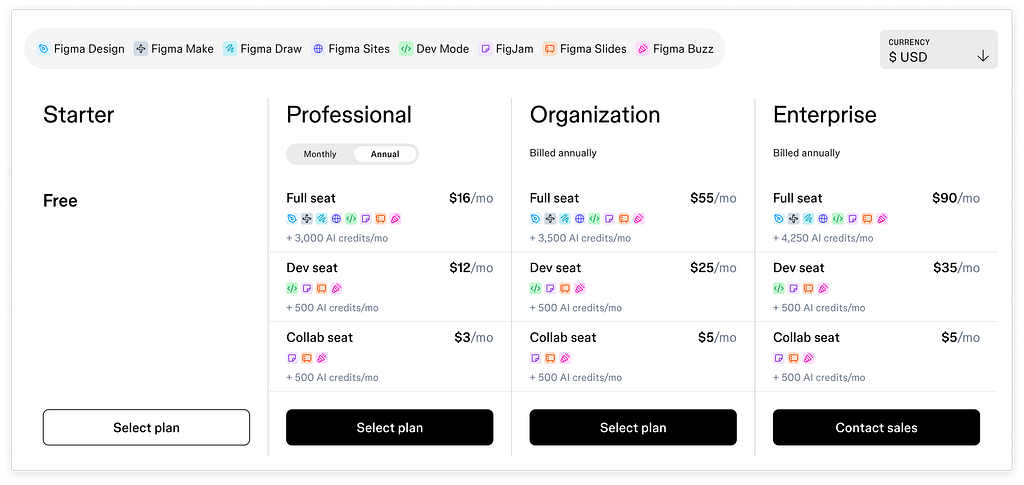

All Figma AI features moved out of beta last year, with a credit system introduced across every plan. At the time of writing, the allocations break down as: 500 credits per month for Starter users, 3,000 for Professional, 3,500 for Organisation, and 4,250 for Enterprise. In March 2026, limits began being enforced for all seat types, with pay-as-you-go overage billing rolling out to all plans in Q2 2026, at $0.03 per credit.

On paper, the credit system is generous enough to try things. In practice, users have reported that 3,000 credits amount to around 45 minutes of work in Figma Make at the advanced model tier.

Figma’s own Help Centre acknowledges that credit consumption for agentic features cannot be predicted in advance. The AI determines what actions it needs to take, and the cost only becomes visible once the task completes. To give a sense of scale: changing a font costs approximately 30 credits. Adding basic interactivity between screens costs 75 or more.

Iterating on a complex prototype, the kind of work that requires multiple prompt-and-adjust cycles, eats through credits quickly. Users on the Figma forum have described dropping from 3,000 to 900 credits in a single short session. One user put it simply:

“Imagine a phone plan that charges you for every word you say. It would completely change the way you talk. You wouldn’t focus on what you need to say, but on how much you can afford to say.”

The credits cover background removal, too. And basic image generation. Features that, in the context of a professional design tool, feel more like basic utilities than premium capability.

The pattern connecting Dev Mode to the AI credit rollout is not coincidental. It’s a tested strategy: introduce, establish dependency, charge. And Figma is not the outlier here.

The playbook, industry-wide

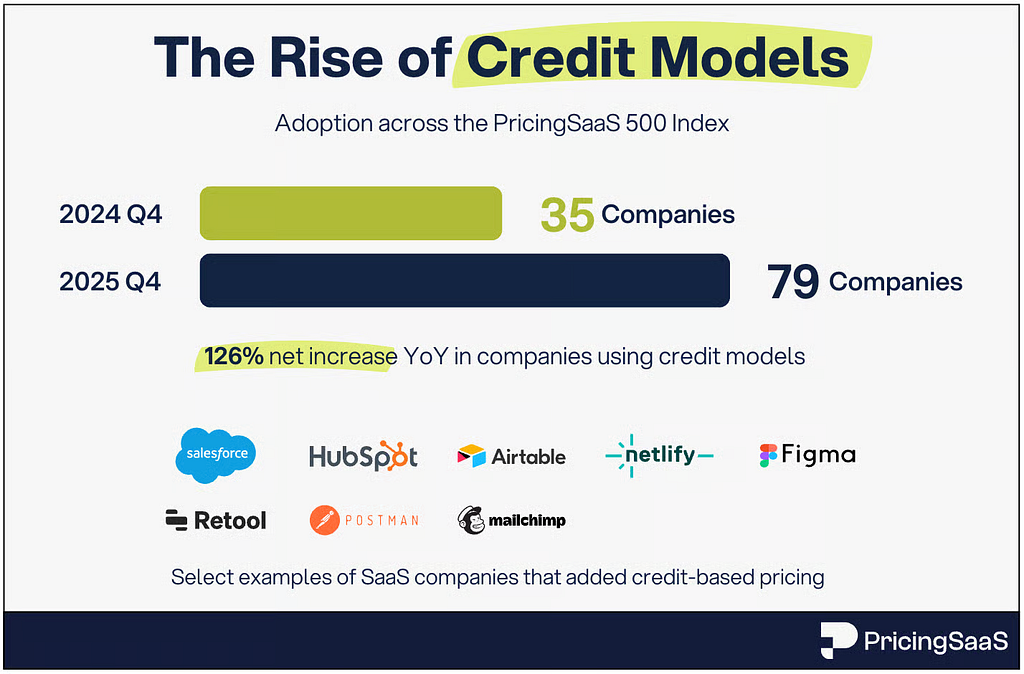

The credit model has become the dominant monetisation mechanism for AI in SaaS. According to data from PricingSaaS, which tracks pricing changes across 500 top SaaS companies, 79 companies had adopted a credit model by the end of 2025. That’s up from 35 at the end of 2024, a 126% year-on-year increase. Figma, HubSpot, and Salesforce all made the switch in the same window.

The rationale is legitimate, and it’s worth acknowledging before reaching for scepticism. AI features carry real marginal costs that traditional SaaS products simply don’t. Running a large language model costs money per request in a way that, say, adding a user to a spreadsheet does not. When models get more capable, they also get more expensive to serve: Anthropic’s Claude Opus 4, for instance, costs $15 per million input tokens and $75 per million output tokens, among the highest rates in the market. Those costs have to go somewhere, and metering systems are businesses’ attempt to pass them on in a structured way while keeping the advertised subscription price unchanged.

But understanding why credit models exist doesn’t mean treating all implementations as equivalent. The same structure can be a tool for transparency or a mechanism for exploitation. And recent history provides some instructive contrasts.

When the meter ran too fast

In June 2025, Cursor, the AI-powered code editor that had grown to over $500 million in annual recurring revenue, announced a pricing update to its $20-per-month Pro plan, framing it as routine.

The change replaced a fixed allowance of 500 fast responses with a dollar-equivalent credit pool, billed at actual API rates. Different models would consume credits at different rates. The plan still said “unlimited” in places, but that now applied only to the Auto mode, which routed to cheaper, less sophisticated models. Using Claude Sonnet or GPT-5.2 directly, the effective monthly request count dropped from around 500 to roughly 225.

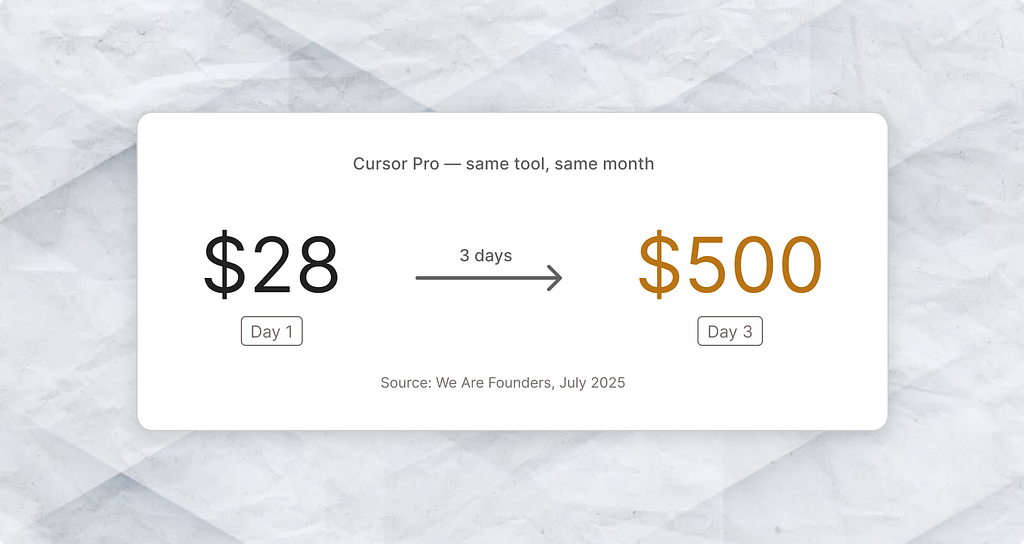

The community response was swift and severe. Users reported their monthly allocation burning through in two or three heavy sessions. Some teams found themselves staring at invoices that reflected hundreds of dollars in unexpected overages, having not understood that exceeding the pool would trigger automatic charges. One user documented costs jumping from $28 to $500 in three days. On Reddit threads and developer forums, the conversation shifted quickly from frustration to something closer to betrayal.

On 4 July 2025, CEO Michael Truell published a public apology:

“We recognise that we didn’t handle this pricing rollout well, and we’re sorry. Our communication was not clear enough and came as a surprise to many of you.”

Refunds were offered for all unexpected charges between 16 June and 4 July. The pricing page was quietly updated to replace “rate limits” with “usage credit pool.”

What’s instructive about the Cursor episode isn’t just that the rollout went badly. It’s why it went badly, and what the community’s reaction revealed. The anger wasn’t primarily about the cost increase itself. It was about the perceived terms being changed mid-relationship, without consent. Developers had structured workflows around the tool. They’d made commitments to clients and projects. When the underlying contract shifted with minimal notice, the breach felt less like a billing adjustment and more like a fundamental violation of trust.

A portion of users migrated to Windsurf, priced at $15 per month, immediately afterwards. Trust, once broken by pricing behaviour, is not easily reassembled by an apology.

Who gets left behind

The credit model creates an asymmetry that’s easy to miss when the discourse focuses on total monthly cost. The real gap isn’t necessarily between a $20 plan and a $40 plan. It’s between users whose employers absorb AI costs as a business expense and those who pay out of pocket. Not to mention teams with predictable, steady workflows and those whose usage shifts with every new project.

For a freelance designer working on Figma Make across multiple client briefs, or a small agency building prototypes under deadline pressure, credit anxiety isn’t abstract. It changes how you work. You ration prompts. You second-guess whether a design iteration is worth the cost. You defer to lower-capability models to conserve credits, even when the advanced models would produce better results. The tool is technically available. The experience of using it freely is not.

This is worth naming as a structural issue rather than a personal one. Credit models that apply the same monthly allocation regardless of user type, enterprise team versus solo practitioner, aren’t neutral. They’re calibrated toward users who can absorb costs and predict usage, at the expense of those who can’t. Platforms benefit from the headline inclusivity of “every seat gets credits” while the practical reality favours a particular tier of user.

The broader market data reinforces this. In 2025, 68% of SaaS platforms with AI features restricted them to premium tiers. AI add-ons have been found to add between 30% and 110% to base costs. Microsoft Copilot, as a straightforward example, requires a Microsoft 365 Business Standard subscription before the Copilot licence can even be added, bringing the minimum effective monthly cost to $42.50 per user. These aren’t edge cases. They’re the shape of the market.

Credits as transitional infrastructure

There is a more charitable reading of where all of this is headed. According to analysts who track SaaS monetisation, the credit model is not intended as a permanent solution. It’s a holding pattern while the industry figures out what it’s actually charging for.

One director of monetisation at a large enterprise productivity company put it plainly in an industry report:

“Credits gave us breathing room while we figured out the real value metric. But they’re not intuitive to buyers.”

That’s an honest admission, and it points toward something real: credits are a proxy for value, not a direct measure of it. They obscure the actual cost of individual actions, which makes them convenient for platforms but difficult to make sense of as a user. What is a credit worth? It depends on the action, the model, the complexity of the task, and which pricing tier you’re on. That lack of clarity is by design. Users can’t easily benchmark the cost of what they’re doing against alternatives.

Some analysts predict that 2026 will see a correction toward simpler, more predictable pricing. Companies like Salesforce have already moved in the direction of output-based credits, where cost is tied to completed actions rather than raw consumption, which at least makes the unit more legible. Others are bundling AI into base pricing rather than metering it altogether, prioritising customer trust over billing precision.

The credit systems flooding the market right now represent the industry’s growing pains, not its destination. Businesses are still working out their cost structures and margin requirements at scale. That much is clear. So is the fact that it’s being transferred, to a significant degree, onto users.

The endowment effect, applied to software

There’s a psychological dimension here that pricing strategy rarely accounts for, but shapes what these transitions actually feel like.

The endowment effect, the well-documented tendency to value things more once we own them, operates in software workflows as much as it does in consumer goods. When a tool becomes embedded in your process, it starts to feel like yours. Not in a proprietary sense, but in the sense that your professional identity and your daily output have formed around it. Figma’s Inspect panel was, for many developers, simply part of how design handoffs happened. Cursor’s Pro plan was part of how developers built things. These weren’t luxuries being reconsidered; they were baselines being moved.

When those baselines shift, the psychological response is disproportionate to the financial cost, because the cost isn’t purely financial. It’s the disruption to a workflow that felt stable. It’s the re-evaluation of a tool relationship that had seemed settled. And for the users who feel this most acutely, the option to “just pay more” doesn’t resolve the underlying discomfort, because the discomfort isn’t merely about the price. It’s about discovering that the foundation was less solid than it appeared.

The platforms that handle this well invest in extensive communication, gradual rollouts, and genuine transparency about what’s changing and why. The ones who don’t, tend to find out about the endowment effect the hard way, via forum revolts and churn spikes.

Reading the pattern

None of this means that AI tool pricing is uniformly cynical, or that the costs are invented. The economics are real. The most advanced models are expensive. Margins in AI-first SaaS are structurally lower than in traditional software, and the pricing structures are still being worked out in real time across the industry.

But “the costs are real” and “this is designed to maximise revenue at the expense of certain user segments” are not mutually exclusive statements. Both can be true simultaneously, and the pattern across Figma, Cursor, and the broader market suggests that the deployment of credit models has frequently prioritised extracting value from embedded users over building sustainable, trust-based pricing relationships.

These aren’t edge cases:

- the freelancer who rations Figma Make prompts to stay within their monthly allocation,

- the developer who migrated to a cheaper tool after Cursor changed the terms,

- the small agency that decided Dev Mode wasn’t worth the licensing cost and built workarounds instead.

They’re the product of a market structure that talks about democratising AI while building pricing systems that concentrate its meaningful benefits toward the users with the deepest pockets.

That’s not a reason to avoid AI tools, or to assume bad faith from every platform announcement. It is a reason to read the beta period not as generosity, but as a calculated step in a sequence. The meter starts running eventually. The question is whether you’ll be able to afford it when it does, and whether you had any say in setting the rate.

Thanks for reading! 📖

If you enjoyed this, follow me on Medium for more on the psychology of design and technology.

References & Credits

- Figma. (2025, December 9). Updates to AI credits in Figma. Figma Blog. https://www.figma.com/blog/updates-to-ai-credits-in-figma/

- Figma Help Centre. (2026). How AI credits work. https://help.figma.com/hc/en-us/articles/33459875669015

- Figma Community Forums. (2025–2026). Figma AI credits; Figma Make AI credit limits not feasible; Dev mode pricing. https://forum.figma.com

- LogRocket Blog. (2024, May 20). Understanding Figma billing with the new payment structure. https://blog.logrocket.com/ux-design/understanding-figma-billing-new-payment-structure/

- Pixso. (2024). Figma Dev Mode BETA pricing raises concerns among users. https://pixso.net/news/figma-dev-mode-pricing/

- TechCrunch. (2025, July 7). Cursor apologises for unclear pricing changes that upset users. https://techcrunch.com/2025/07/07/cursor-apologizes-for-unclear-pricing-changes-that-upset-users/

- We Are Founders. (2025, July 11). Cursor’s pricing disaster: how a “routine update” turned into a developer exodus. https://www.wearefounders.uk/cursors-pricing-disaster-how-a-routine-update-turned-into-a-developer-exodus/

- Growth Unhinged. (2026, February 4). What actually works in SaaS pricing right now. https://www.growthunhinged.com/p/2025-state-of-saas-pricing-changes

- BetterCloud. (2026, January 21). AI and the SaaS industry in 2026. https://www.bettercloud.com/monitor/saas-industry/

- AIonX. (2026). AI pricing comparison 2026: ChatGPT vs Claude vs Gemini. https://aionx.co/ai-comparisons/ai-pricing-comparison/

- Ibbaka. (2025, September 11). Four perspectives on credit-based pricing for AI agents. https://www.ibbaka.com/ibbaka-market-blog/four-perspectives-on-credit-based-pricing-for-ai-agents

- Metronome. (2025). AI pricing in practice: 2025 field report from leading SaaS teams. https://metronome.com/blog/ai-pricing-in-practice-2025-field-report-from-leading-saas-teams

- Aakash G. (2026). How to price AI products: the complete guide for PMs. https://www.news.aakashg.com/p/how-to-price-ai-products

- Getmonetizely. (2025, July 23). Cursor AI’s $1B SaaS pricing crisis: a strategy gone wrong. https://www.getmonetizely.com/blogs/cursor-ais-billion-dollar-saas-pricing-fiasco

Who can actually afford AI tools now? was originally published in UX Collective on Medium, where people are continuing the conversation by highlighting and responding to this story.